Keith Dicker

IceCap : August 2015

Governments all around the world have borrowed too much money and the weight of these debts are choking economic growth.

And to make matters worse – these very same governments and their central banks have implemented various plans that have only made matters worse.

The global debt crisis has escalated to a point where the government bond bubble has inflated itself to become the mother of all bubbles. It’s going to burst, and when it does it wont be pretty.

Further evidence to support our view is as follows:

Canada – the collapse in oil and commodity markets has pushed the country into recession and the Canadian Dollar to decline to levels lower than that reached during the 2008 crisis.

Oil dependent provinces Alberta and Newfoundland remain in deep denial. Since everyone in these provinces have only ever experienced a booming oil market, many naively believe things will bounce back – and quickly.

Meanwhile, both Toronto and Vancouver housing markets also remain in denial as they continue to go gangbusters. Buyers today are likely buying at all-time highs.

And as we predicted last year, the Bank of Canada has cut (not raised) interest rates twice in the last 6 months.

We fully expect the Bank of Canada to eventually cut interest rates to 0% and start a money printing program as well. And for the stunner – NEGATIVE interest rates will not be that far behind.

Australia – Over the last 20 years, China has been viewed as the growth engine of the world, and justifiably so. With annual growth rates between 8% to 15%, China’s economy was literally eating every rock, stalk and barrel of practically every commodity in the world.

And naturally, any country or company that produced these commodities made a tonne of money – including Australia.

Today, China’s growth rate has slowed to about 3% which is a dramatic slow down compared to what it achieved in the past. This slowdown and China’s effort to even maintain these rates, will have significant repercussions around the world.

And the first up to bear the brunt of this slowdown is its closest supplier of raw materials – Australia.

With dark clouds on the economic horizon, the Australian government and central bank is doing everything possible to prevent the unpreventable recession.

Interest rates have been reduced to all-time historical lows, meanwhile the Australian Dollar has plummeted -25% over the last year. Yet – the negative outlook has not improved.

Brazil – Like Australia, Brazil has benefitted immensely from China’s growth. And now, also like Australia, it too is feeling the affects of the dramatic Chinese slowdown.

The economy has now declined for 12 consecutive months making it both the longest and deepest recession in 25 years.

But wait – it gets worse. Despite declining growth, inflation continues to soar higher causing interest rates to rise as well.

And if that wasn’t bad, also know that the Brazilian currency has fell off the cliff at -53%.

Sweden – Unlike Australia and Brazil, Sweden relies very little on China as a buyer of last resort. Yet, the Swedish economy is also not very hot these days.

In fact, instead of spectacular and dramatic declines in anything, it is doing the exact opposite – it just isn’t moving.

While Sweden isn’t in the Eurozone, it is smack dab next to it and that in itself is reason enough for the lack of growth. We’ve written before how the debt crisis in the Eurozone is acting like a giant, slow moving tornado that is sucking the life out of the economy and everything near by. And unfortunately for Sweden, it is very near by.

While economic growth in the Nordic state hasn’t declined, it hasn’t accelerated either – and this is what has many worried.

So worried, that the central bank shocked everyone not once but twice, by first announcing that they would begin to print money, and then when they announced that interest rates would be NEGATIVE.

These actions are so severe, that we need to repeat them:

1) MONEY PRINTING

2) NEGATIVE INTEREST RATES

It is hoped that these actions will cause people and companies to loosen their wallets and start spending again. Yet, what the government and the central bank doesn’t understand is that these actions will actually make the problem worse.

As the global economy continues to move as we expect, there is nothing Sweden can do to change what is coming – a global recession and a significantly weaker Krona.

China, Australia, Brazil, Canada, Sweden – it is beyond us how anyone can declare the crisis isn’t spreading.

* * *

IceCap’s full letter below

Greek “Hell” Remains After Athens Uses Creditor Money To Repay Creditors

Zero Hedge: July 20, 2015

Earlier today, Greece used up virtually its entire €7.1 billion bridge loan from the EU to repay its creditors: between the money due to the ECB, the arrears to the IMF and the cash borrowed from the Greek central bank, Athens had about €300 million left over from the entire inbound wire to use as it sees fit just hours after the money was received, and then promptly sent right back.

Or, as some put it, Greece collected a 4% transaction fee for facilitating a €6.8 billion payment from its creditors to its creditors.

So does this mean things are “fixed” in Greece, if only temporarily? Not exactly, as the following table shows, there is exactly one month until the next €3.2 billion payment is due to the ECB. So unless Europe finalizes the terms of the third €86 billion EFSF bailout in the next 4 weeks, Greece will need another bridge loan just to repay the ECB.

Ok, but if Greece somehow survives until the end of 2015 despite a new government and with blistering VAT hikes, even as bank lines to withdraw money refuse to go away, then will it finally be ok?

Well, no.

As we showed before when we showed the various Greek circle of debt hell, unless Greece finds a way to access the market once again following its “triumphal return” in mid-2014 when it issued bonds that cost investors (with other people’s money) their 2015 bonus, it is only then that the Greek debt repayment hell begins.

(read the full article at zero hedge)

How Goldman Sachs Profited From the Greek Debt Crisis

Robert B. Reich

The Nation : July 16, 2015

The investment bank made millions by helping to hide the true extent of the debt, and in the process almost doubled it.

The Greek debt crisis offers another illustration of Wall Street’s powers of persuasion and predation, although the Street is missing from most accounts.

The crisis was exacerbated years ago by a deal with Goldman Sachs, engineered by Goldman’s current CEO, Lloyd Blankfein. Blankfein and his Goldman team helped Greece hide the true extent of its debt, and in the process almost doubled it. And just as with the American subprime crisis, and the current plight of many American cities, Wall Street’s predatory lending played an important although little-recognized role.

In 2001, Greece was looking for ways to disguise its mounting financial troubles. The Maastricht Treaty required all eurozone member states to show improvement in their public finances, but Greece was heading in the wrong direction. Then Goldman Sachs came to the rescue, arranging a secret loan of 2.8 billion euros for Greece, disguised as an off-the-books “cross-currency swap”—a complicated transaction in which Greece’s foreign-currency debt was converted into a domestic-currency obligation using a fictitious market exchange rate.

As a result, about 2 percent of Greece’s debt magically disappeared from its national accounts. Christoforos Sardelis, then head of Greece’s Public Debt Management Agency, later described the deal to Bloomberg Business as “a very sexy story between two sinners.” For its services, Goldman received a whopping 600 million euros ($793 million), according to Spyros Papanicolaou, who took over from Sardelis in 2005. That came to about 12 percent of Goldman’s revenue from its giant trading and principal-investments unit in 2001—which posted record sales that year. The unit was run by Blankfein.

Then the deal turned sour. After the 9/11 attacks, bond yields plunged, resulting in a big loss for Greece because of the formula Goldman had used to compute the country’s debt repayments under the swap. By 2005, Greece owed almost double what it had put into the deal, pushing its off-the-books debt from 2.8 billion euros to 5.1 billion. In 2005, the deal was restructured and that 5.1 billion euros in debt locked in. Perhaps not incidentally, Mario Draghi, now head of the European Central Bank and a major player in the current Greek drama, was then managing director of Goldman’s international division.

Greece wasn’t the only sinner. Until 2008, European Union accounting rules allowed member nations to manage their debt with so-called off-market rates in swaps, pushed by Goldman and other Wall Street banks. In the late 1990s, JPMorgan enabled Italy to hide its debt by swapping currency at a favorable exchange rate, thereby committing Italy to future payments that didn’t appear on its national accounts as future liabilities.

But Greece was in the worst shape, and Goldman was the biggest enabler. Undoubtedly, Greece suffers from years of corruption and tax avoidance by its wealthy. But Goldman wasn’t an innocent bystander: It padded its profits by leveraging Greece to the hilt—along with much of the rest of the global economy. Other Wall Street banks did the same. When the bubble burst, all that leveraging pulled the world economy to its knees.

[…]

Meanwhile, cities and states across America have been forced to cut essential services because they’re trapped in similar deals sold to them by Wall Street banks. Many of these deals have involved swaps analogous to the ones Goldman sold the Greek government. And much like the assurances it made to the Greek government, Goldman and other banks assured the municipalities that the swaps would let them borrow more cheaply than if they relied on traditional fixed-rate bonds—while downplaying the risks they faced. Then, as interest rates plunged and the swaps turned out to cost far more, Goldman and the other banks refused to let the municipalities refinance without paying hefty fees to terminate the deals.

Three years ago, the Detroit Water Department had to pay Goldman and other banks penalties totaling $547 million to terminate costly interest-rate swaps. Forty percent of Detroit’s water bills still go to paying off the penalty. Residents of Detroit whose water has been shut off because they can’t pay have no idea that Goldman and other big banks are responsible. Likewise, the Chicago school system—whose budget is already cut to the bone—must pay over $200 million in termination penalties on a Wall Street deal that had Chicago schools paying $36 million a year in interest-rate swaps.

A deal involving interest-rate swaps that Goldman struck with Oakland, California, more than a decade ago has ended up costing the city about $4 million a year, but Goldman has refused to allow Oakland out of the contract unless it ponies up a $16 million termination fee—prompting the city council to pass a resolution to boycott Goldman. When confronted at a shareholder meeting about it, Blankfein explained that it was against shareholder interests to tear up a valid contract.

Goldman Sachs and the other giant Wall Street banks are masterful at selling complex deals by exaggerating their benefits and minimizing their costs and risks. That’s how they earn giant fees. When a client gets into trouble—whether that client is an American homeowner, a US city, or Greece—Goldman ducks and hides behind legal formalities and shareholder interests.

Borrowers that get into trouble are rarely blameless, of course: They spent too much, and were gullible or stupid enough to buy Goldman’s pitches. Greece brought on its own problems, as did many American homeowners and municipalities.

But in all of these cases, Goldman knew very well what it was doing. It knew more about the real risks and costs of the deals it proposed than those who accepted them. “It is an issue of morality,” said the shareholder at the Goldman meeting where Oakland came up. Exactly.

(Full article at The Nation)

Greece Is Just The Beginning: The 21st Century ‘Enclosures’ Have Begun

Paul Craig Roberts : July 15, 2015

All of Europe, and insouciant Americans and Canadians as well, are put on notice by Syriza’s surrender to the agents of the One Percent. The message from the collapse of Syriza is that the social welfare system throughout the West will be dismantled.

The Greek prime minister Alexis Tsipras has agreed to the One Percent’s looting of the Greek people of the advances in social welfare that the Greeks achieved in the post-World War II 20th century. Pensions and health care for the elderly are on the way out. The One Percent needs the money.

The protected Greek islands, ports, water companies, airports, the entire panoply of national patrimony, is to be sold to the One Percent. At bargain prices, of course, but the subsequent water bills will not be bargains.

This is the third round of austerity imposed on Greece, austerity that has required the complicity of the Greeks’ own governments. The austerity agreements serve as a cover for the looting of the Greek people literally of everything. The IMF is one member of the Troika that is imposing the austerity, despite the fact that the IMF’s economists have said that the austerity measures have proven to be a mistake. The Greek economy has been driven down by the austerity. Therefore, Greece’s indebtedness has increased as a burden. Each round of austerity makes the debt less payable.

But when the One Percent is looting, facts are of no interest. The austerity, that is the looting, has gone forward despite the fact that the IMF’s economists cannot justify it.

Greek democracy has proven itself to be impotent. The looting is going forward despite the vote one week ago by the Greek people rejecting it. So what we observe in Alexis Tsipras is an elected prime minister representing not the Greek people but the One Percent.

The One Percent’s sigh of relief has been heard around the world. The last European leftist party, or what passes as leftist, has been brought to heel, just like Britain’s Labour Party, the French Socialist Party, and all the rest.

Without an ideology to sustain it, the European left is dead (read the full article at Paul Craig Roberts)

The Euro-Summit ‘Agreement’ on Greece – annotated by Yanis Varoufakis

Yanis Varoufakis

July 15, 2015

The Euro Summit statement (or Terms of Greece’s Surrender – as it will go down in history) follows, annotated by yours truly. The original text is untouched with my notes confined to square brackets (and in red). Read and weep… [For a pdf copy click here.]

Euro Summit Statement Brussels, 12 July 2015

The Euro Summit stresses the crucial need to rebuild trust with the Greek authorities [i.e. the Greek government must introduce new stringent austerity directed at the weakest Greeks that have already suffered grossly] as a pre- requisite for a possible future agreement on a new ESM programme [i.e. for a new extend-and-pretend loan].

In this context, the ownership by the Greek authorities is key [i.e. the Syriza government must sign a declaration of having defected to the troika’s ‘logic’], and successful implementation should follow policy commitments.

A euro area Member State requesting financial assistance from the ESM is expected to address, wherever possible, a similar request to the IMF This is a precondition for the Eurogroup to agree on a new ESM programme. Therefore Greece will request continued IMF support (monitoring and financing) from March 2016 [i.e. Berlin continues to believe that the Commission cannot be trusted to ‘police’ Europe’s own ‘bailout’ programs].

Given the need to rebuild trust with Greece, the Euro Summit welcomes the commitments of the Greek authorities to legislate without delay a first set of measures [i.e. Greece must subject itself to fiscal waterboarding, even before any financing is offered]. These measures, taken in full prior agreement with the Institutions, will include:

By 15 July

- the streamlining of the VAT system [i.e. making it more regressive, through rate rises that encourage more VAT evasion]and the broadening of the tax base to increase revenue [i.e. dealing a major blow at the only Greek growth industry – tourism].

- upfront measures to improve long-term sustainability of the pension system as part of a comprehensive pension reform programme [i.e. reducing the lowest of the low of pensions, while ignoring that the depletion of pension funds’ capital due to the 2012 troika-designed PSI and the ill effects of low employment & undeclared paid labour].

- the safeguarding of the full legal independence of ELSTAT [i.e. the troika demands complete control of the way Greece’s budget balance is computed, with a view to controlling fully the magnitude of austerity it imposes on the government.]

- full implementation of the relevant provisions of the Treaty on Stability, Coordination and Governance in the Economic and Monetary Union, in particular by making the Fiscal Council operational before finalizing the MoU and introducing quasi-automatic spending cuts in case of deviations from ambitious primary surplus targets after seeking advice from the Fiscal Council and subject to prior approval of the Institutions [i.e. the Greek government, which knows that the imposed fiscal targets will never be achieved under the imposed austerity, must commit to further, automated austerity as a result of the troika’s newest failures.]

By 22 July

- the adoption of the Code of Civil Procedure, which is a major overhaul of procedures and arrangements for the civil justice system and can significantly accelerate the judicial process and reduce costs [i.e. foreclosures, evictions and liquidation of thousands of homes and businesses who are not in a position to keep up with their mortgages/loans.]

- the transposition of the BRRD with support from the European Commission.

Immediately, and only subsequent to legal implementation of the first four above-mentioned measures as well as endorsement of all the commitments included in this document by the Greek Parliament, verified by the Institutions and the Eurogroup, may a decision to mandate the Institutions to negotiate a Memorandum of Understanding (MoU) be taken [i.e. The Syriza government must be humiliated to the extent that it is asked to impose harsh austerity upon itself as a first step towards requesting another toxic bailout loan, of the sort that Syriza became internationally famous for opposing.]

This decision would be taken subject to national procedures having been completed and if the preconditions of Article 13 of the ESM Treaty are met on the basis of the assessment referred to in Article 13.1. In order to form the basis for a successful conclusion of the MoU, the Greek offer of reform measures needs to be seriously strengthened to take into account the strongly deteriorated economic and fiscal position of the country during the last year [i.e. the Syriza government must accept the lie that it, and not the asphyxiation tactics of the creditors, caused the sharp economic deterioration of the past six months – the victim is being asked to take the blame by the on behalf of the villain.]

The Greek government needs to formally commit to strengthening their proposals [i.e. to make them more regressive and more inhuman] in a number of areas identified by the Institutions, with a satisfactory clear timetable for legislation and implementation, including structural benchmarks, milestones and quantitative benchmarks, to have clarity on the direction of policies over the medium-run. They notably need, in agreement with the Institutions, to:

- carry out ambitious pension reforms [i.e. cuts] and specify policies to fully compensate for the fiscal impact of the Constitutional Court ruling on the 2012 pension reform [i.e. cancel the Court’s decision in favour of pensioners] and to implement the zero deficit clause [i.e. cut by 85% the secondary pensions that the Syriza government fought tooth and nail to preserve over the past five months] or mutually agreeable alternative measures [i.e. find ‘equivalent’ victims] by October 2015;

- adopt more ambitious product market reforms with a clear timetable for implementation of all OECD toolkit I recommendations [i.e. the recommendations that the OECD has now renounced after having re-designed these reforms in collaboration with the Syriza government], including Sunday trade, sales periods, pharmacy ownership, milk and bakeries, except over-the-counter pharmaceutical products, which will be implemented in a next step, as well as for the opening of macro-critical closed professions (e.g. ferry transportation). On the follow-up of the OECD toolkit-II, manufacturing needs to be included in the prior action;

- on energy markets, proceed with the privatisation of the electricity transmission network operator (ADMIE), unless replacement measures can be found that have equivalent effect on competition, as agreed by the Institutions [i.e. ADMIE will be sold off to specific foreign vested interests at the behest of the Institutions.]

- on labour markets, undertake rigorous reviews and modernisation of collective bargaining [i.e. to make sure that no collective bargaining is allowed], industrial action [i.e. that must be banned] and, in line with the relevant EU directive and best practice, collective dismissals [i.e. that should be allowed at the employers’ whim], along the timetable and the approach agreed with the Institutions [i.e. the Troika decides.]

On the basis of these reviews, labour market policies should be aligned with international and European best practices, and should not involve a return to past policy settings which are not compatible with the goals of promoting sustainable and inclusive growth [i.e. there should be no mechanisms that waged labour can use to extract better conditions from employers.]

- adopt the necessary steps to strengthen the financial sector, including decisive action on non-performing loans [i.e. a tsunami of foreclosures is ante portas] and measures to strengthen governance of the HFSF and the banks [i.e. the Greek people who maintain the HFSF and the banks will have precisely zero control over the HFSF and the banks.], in particular by eliminating any possibility for political interference especially in appointment processes. [i.e. except the political interference of the Troika.] On top of that, the Greek authorities shall take the following actions:

- to develop a significantly scaled up privatisation programme with improved governance; valuable Greek assets will be transferred to an independent fund that will monetize the assets through privatisations and other means [i.e. an East German-like Treuhand is envisaged to sell off all public property but without the equivalent large investments that W. Germany put into E. Germany in compensation for the Treuhand disaster.] The monetization of the assets will be one source to make the scheduled repayment of the new loan of ESM and generate over the life of the new loan a targeted total of EUR 50bn of which EUR 25bn will be used for the repayment of recapitalization of banks and other assets and 50 % of every remaining euro (i.e. 50% of EUR 25bn) will be used for decreasing the debt to GDP ratio and the remaining 50 % will be used for investments [i.e. public property will be sold off and the pitiful sums will go toward servicing an un-serviceable debt – with precisely nothing left over for public or private investments.] This fund would be established in Greece and be managed by the Greek authorities under the supervision of the relevant European Institutions [i.e. it will be nominally in Greece but, just like the HFSF or the Bank of Greece, it will be controlled fully by the creditors.] In agreement with Institutions and building on best international practices, a legislative framework should be adopted to ensure transparent procedures and adequate asset sale pricing, according to OECD principles and standards on the management of State Owned Enterprises (SOEs) [i.e. the Troika will do what it likes.]

- in line with the Greek government ambitions, to modernise and significantly strengthen the Greek administration, and to put in place a programme, under the auspices of the European Commission, for capacity-building and de-politicizing the Greek administration [i.e. Turning Greece into a democracy-free zone modelled on Brussels, a form of supposedly technocratic government, which is politically toxic and macro-economically inept] A first proposal should be provided by 20 July after discussions with the Institutions. The Greek government commits to reduce further the costs of the Greek administration [i.e. to reduce the lowest wages while increasing a little the wages some of the Troika-friendly apparatchiks], in line with a schedule agreed with the Institutions.

- to fully normalize working methods with the Institutions, including the necessary work on the ground in Athens, to improve programme implementation and monitoring [i.e. The Troika strikes back and demands that the Greek government invite it to return to Athens as Conqueror – the Carthaginian Peace in all its glory.] The government needs to consult and agree with the Institutions on all draft legislation in relevant areas with adequate time before submitting it for public consultation or to Parliament [i.e. Greek Parliament must, again, after five months of short-lived independence, become an appendage of the Troika – passing translated legislation mechanistically.] The Euro Summit stresses again that implementation is key, and in that context welcomes the intention of the Greek authorities to request by 20 July support from the Institutions and Member States for technical assistance, and asks the European Commission to coordinate this support from Europe;

- With the exception of the humanitarian crisis bill, the Greek government will reexamine with a view to amending legislations that were introduced counter to the February 20 agreement by backtracking on previous programme commitments or identify clear compensatory equivalents for the vested rights that were subsequently created [i.e. In addition to promising that it will no longer legislative autonomously, the Greek government will retrospectively annul all Bills it passed over the past five months.]

The above-listed commitments are minimum requirements to start the negotiations with the Greek authorities. However, the Euro Summit made it clear that the start of negotiations does not preclude any final possible agreement on a new ESM programme, which will have to be based on a decision on the whole package (including financing needs, debt sustainability and possible bridge financing) [i.e. self-flagellate, impose further austerity upon an economy crushed by austerity, and then we shall see whether the Eurogroup will grave you with another toxic, unsustainable loans.]

The Euro Summit takes note of the possible programme financing needs of between EUR 82 and 86bn, as assessed by the Institutions [i.e. the Eurogroup conjured up a huge number, well above what is necessary, in order to signal the debt restructuring is out and that debt bondage ad infinitum is the name of the game.] It invites the Institutions to explore possibilities to reduce the financing envelope, through an alternative fiscal path or higher privatisation proceeds [i.e. And, yes, it may possible that pigs will fly.] Restoring market access, which is an objective of any financial assistance programme, lowers the need to draw on the total financing envelope [i.e. which is something the creditors will do their utmost to avoid, e.g. by ensuring that Greece will only enter the ECB’s quantitative easing program in 2018, once quantitative easing is… over.]

The Euro Summit takes note of the urgent financing needs of Greece which underline the need for very swift progress in reaching a decision on a new MoU: these are estimated to amount to EUR 7bn by 20 July and an additional EUR 5bn by mid August [i.e. Extend and Pretend gets another spin.] The Euro Summit acknowledges the importance of ensuring that the Greek sovereign can clear its arrears to the IMF and to the Bank of Greece and honour its debt obligations in the coming weeks to create conditions which allow for an orderly conclusion of the negotiations. The risks of not concluding swiftly the negotiations remain fully with Greece [i.e. Once more, demanding that the victim takes all the blame in behalf of the villain.] The Euro Summit invites the Eurogroup to discuss these issues as a matter of urgency.

Given the acute challenges of the Greek financial sector, the total envelope of a possible new ESM programme would have to include the establishment of a buffer of EUR 10 to 25bn for the banking sector in order to address potential bank recapitalisation needs and resolution costs, of which EUR 10bn would be made available immediately in a segregated account at the ESM [i.e. the Troika admits that the 2013-14 recapitalisation of the banks, which would only need a top up of at most 10 billion, was insufficient – but, of course, blames it on… the Syriza government.]

The Euro Summit is aware that a rapid decision on a new programme is a condition to allow banks to reopen, thus avoiding an increase in the total financing envelope [i.e. The Troika closed Greece’s banks to force the Syriza government to capitulate and now cries out for their re-opening.] The ECB/SSM will conduct a comprehensive assessment after the summer. The overall buffer will cater for possible capital shortfalls following the comprehensive assessment after the legal framework is applied.

There are serious concerns regarding the sustainability of Greek debt [N.b. Really? Gosh!] This is due to the easing of policies during the last twelve months, which resulted in the recent deterioration in the domestic macroeconomic and financial environment [i.e. It is not the Extend and Pretend ‘bailout’ loans of 2010 and 2012 that, in conjunction with GDP-sapping austerity, caused the debt to scale immense heights – it was the prospect, and reality, of a government that criticized the the Extend and Pretend ‘bailout’ loans that… caused Debt’s Unustainability!]

The Euro Summit recalls that the euro area Member States have, throughout the last few years, adopted a remarkable set of measures supporting Greece’s debt sustainability, which have smoothed Greece’s debt servicing path and reduced costs significantly [i.e. The 1st & 2nd ‘bailout’ programs failed, the debt skyrocketing as it was always going to since the real purpose of the ‘bailout’ programs was to transfer banking losses to Europe’s taxpayers.] Against this background, in the context of a possible future ESM programme, and in line with the spirit of the Eurogroup statement of November 2012 [i.e. a promise of debt restructure to the previous Greek government was never kept by the creditors], the Eurogroup stands ready to consider, if necessary, possible additional measures (possible longer grace and payment periods) aiming at ensuring that gross financing needs remain at a sustainable level. These measures will be conditional upon full implementation of the measures to be agreed in a possible new programme and will be considered after the first positive completion of a review [i.e. Yet again, the Troika shall let the Greek government labour under un-payable debt and when, as a result, the program fails, poverty rises further and incomes collapse much more, then we may haircut some of the debt – as the Troika did in 2012.]

The Euro Summit stresses that nominal haircuts on the debt cannot be undertaken [N.b. The Syriza government has been suggesting, since January, a moderate debt restructure, with no haircuts, maximizing the expected net present value of Greece’s repayments to creditors’ – which was rejected by the Troika because their aim was, simply, to humiliate Syriza.] Greek authorities reiterate their unequivocal commitment to honour their financial obligations to all their creditors fully and in a timely manner [N.b. Which can only happen after a substantial debt restrucuture.] Provided that all the necessary conditions contained in this document are fulfilled, the Eurogroup and ESM Board of Governors may, in accordance with Article 13.2 of the ESM Treaty, mandate the Institutions to negotiate a new ESM programme, if the preconditions of Article 13 of the ESM Treaty are met on the basis of the assessment referred to in Article 13.1. To help support growth and job creation in Greece (in the next 3-5 years) [N.b. Having already destroyed growth and jobs for the past five years…] the Commission will work closely with the Greek authorities to mobilise up to EUR 35bn (under various EU programmes) to fund investment and economic activity, including in SMEs [i.e. Will use the same order of magnitude of structural funds, plus some fantasy money, as were available in 2010-2014.] As an exceptional measure and given the unique situation of Greece the Commission will propose to increase the level of pre-financing by EUR 1bn to give an immediate boost to investment to be dealt with by the EU co-legislators [i.e. Of the headline 35 billion, consider 1 billion as real money.] The Investment Plan for Europe will also provide funding opportunities for Greece [i.e. the same plan that most Eurozone ministers of finance refer to as a phantom program].

(Source: Yanis Varoufakis)

When Wall Street offers free money, watch out

By Allan Sloan and Cezary Podkul

The Washington Post & ProPublica : July 11, 2015

If there were ever a time not to bet the moon on the stock and bond markets, it’s now, with U.S. stocks at near-record highs and interest rates on quality bonds at near-record lows. But Wall Street is urging state and local governments to do just that — and they’re listening.

Despite the risks, governments are lining up to issue billions of dollars in new debt to replenish their depleted pension funds and, as a bonus, take some pressure off strapped budgets. In some cases, the borrowing makes their balance sheets look vastly better. Bankers, who make fat fees for raising the money, are encouraging this borrow-and-bet trend. Their sales pitch is that borrowing at today’s low interest rates all but guarantees a profit for the governments because they can invest the proceeds in their pension funds and for decades earn returns higher than the 5 percent or so in interest that they will pay on the bonds.

But there’s a catch: If the timing is wrong, these so-called pension obligation bonds could clobber the finances of the government issuers. Pension funds and beneficiaries will be better off because pensions will be more soundly financed. But taxpayers — present and future — might be considerably worse off. They will be running huge risks and could get stuck with a massive tab.

“It’s sold as a magic bean,” said Todd Ely, a professor at the University of Colorado at Denver who has studied pension bonds. “But when it goes bad, it’s not free. Then it isn’t really magic. If it could be counted on to work as often as it’s supposed to, then everyone would be doing it.”

Plenty of takers are bellying up to the borrowing bar. Governments sold $670 million worth of pension bonds through the first half of this year, more than double the $300 million raised for all of last year, according to deal-trackers at Thomson Reuters.

That total would more than double if Kansas completes a pending $1 billion deal, which would be its biggest bond issue. A $3 billion sale is under consideration in Pennsylvania, that state’s largest as well. Lawmakers recently rejected record multibillion-dollar deals in Kentucky and Colorado, but those proposals are expected to resurface. And new proposals are being pitched to other governments.

Pension bonds have waxed and waned since the 1980s, but the current boom is different. An examination by The Washington Post and ProPublica found that it’s being driven not only by the prospect of investment profits but also by a new accounting quirk that has largely escaped public notice while morphing into a major marketing tool for Wall Street banks.

The quirk stems from a rule change that was meant to force governments to more clearly disclose the health of their pension funds. But a side effect is to allow governments with extremely underfunded pensions to slash reported shortfalls by $2 or more for each $1 borrowed.

(read the full article at Washington Post)

—

Alternative Free Press -fair use-

Crony Eric Holder Returns as Hero to Law Firm That Lobbies for Big Banks

Lee Fang

The Intercept : July 6, 2015

After failing to criminally prosecute any of the financial firms responsible for the market collapse in 2008, former Attorney General Eric Holder is returning to Covington & Burling, a corporate law firm known for serving Wall Street clients.

The move completes one of the more troubling trips through the revolving door for a cabinet secretary. Holder worked at Covington from 2001 right up to being sworn in as attorney general in Feburary 2009. And Covington literally kept an office empty for him, awaiting his return.

The Covington & Burling client list has included four of the largest banks, including Bank of America, Citigroup, JPMorgan Chase and Wells Fargo. Lobbying records show that Wells Fargo is still a client of Covington. Covington recently represented Citigroup over a civil lawsuit relating to the bank’s role in Libor manipulation.

Covington was also deeply involved with a company known as MERS, which was later responsible for falsifying mortgage documents on an industrial scale. “Court records show that Covington, in the late 1990s, provided legal opinion letters needed to create MERS on behalf of Fannie Mae, Freddie Mac, Bank of America, JPMorgan Chase and several other large banks,” according to an investigation by Reuters.

The Department of Justice under Holder not only failed to pursue criminal prosecutions of the banks responsible for the mortage meltdown, but in fact de-prioritized investigations of mortgage fraud, making it the “lowest-ranked criminal threat,” according to an inspector general report.

For insiders, the Holder decision to return to Covington was never a mystery. Timothy Hester, the chairman of Covington, told the National Law Journal that Holder’s return to the firm had been “a project” of his ever since Holder left to the join the administration in 2009. When the firm moved to a new building last year, it kept an 11th-story corner office reserved for Holder.

[…]

As Covington prepared for Holder’s return, the firm continued to represent clients before the Department of Justice. For instance, Covington negotiated with the department on behalf of GlaxoSmithKline for a plea agreement in 2010.

Holder’s critics charge that he made a career out of institutionalizing “Too Big to Prosecute” rules within the department. In 1999, as a deputy attorney general, Holder authored a memo arguing that officials should consider the “collateral consequences” when prosecuting corporate crimes. In 2012, Holder’s enforcement chief, Lanny Breuer, admitted during a speech to the New York City Bar Association that the department may go easy on certain corporate criminals if they believe prosecutions may disrupt financial markets or cause layoffs. “In some cases, the health of an industry or the markets are a real factor,” Breuer said.

Rather than face accountability for their failures, the incentive structure of modern Washington is designed to reward both men. Breuer left the department in 2013 to rejoin Covington. Holder is set to become among the highest-earning partners at the firm, with compensation in the seven or eight figures.

(read the full article at The Intercept)

Greece — The One Biggest Lie You Are Being Told By The Media

Truth & Satire: July 3, 2015

Every single mainstream media has the following narrative for the economic crisis in Greece: the government spent too much money and went broke; the generous banks gave them money, but Greece still can’t pay the bills because it mismanaged the money that was given. It sounds quite reasonable, right?

Except that it is a big fat lie … not only about Greece, but about other European countries such as Spain, Portugal, Italy and Ireland who are all experiencing various degrees of austerity. It was also the same big, fat lie that was used by banks and corporations to exploit many Latin American, Asian and African countries for many decades.

Greece did not fail on its own. It was made to fail.

In summary, the banks wrecked the Greek government, and then deliberately pushed it into unsustainable debt … while revenue-generating public assets were sold off to oligarchs and international corporations. The rest of the article is about how and why.

If you are a fan of mafia movies, you know how the mafia would take over a popular restaurant. First, they would do something to disrupt the business – stage a murder at the restaurant or start a fire. When the business starts to suffer, the Godfather would generously offer some money as a token of friendship. In return, Greasy Thumb takes over the restaurant’s accounting, Big Joey is put in charge of procurement, and so on. Needless to say, it’s a journey down a spiral of misery for the owner who will soon be broke and, if lucky, alive.

Now, let’s map the mafia story to international finance in four stages.

Stage 1: The first and foremost reason that Greece got into trouble was the “Great Financial Crisis” of 2008 that was the brainchild of Wall Street and international bankers. If you remember, banks came up with an awesome idea of giving subprime mortgages to anyone who can fog a mirror. They then packaged up all these ticking financial bombs and sold them as “mortgage-backed securities” for a huge profit to various financial entities in countries around the world.

A big enabler of this criminal activity was another branch of the banking system, the group of rating agencies – S&P, Fitch and Moody’s – who gave stellar ratings to these destined-to-fail financial products. Unscrupulous politicians such as Tony Blair joined Goldman Sachs and peddled these dangerous securities to pension funds and municipalities and countries around Europe. Banks and Wall Street gurus made hundreds of billions of dollars in this scheme.

But this was just Stage 1 of their enormous scam. There was much more profit to be made in the next three stages!

Stage 2 is when the financial time bombs exploded. Commercial and investment banks around the world started collapsing in a matter of weeks. Governments at local and regional level saw their investments and assets evaporate. Chaos everywhere!

Vultures like Goldman Sachs and other big banks profited enormously in three ways: one, they could buy other banks such as Lehman brothers and Washington Mutual for pennies on the dollar. Second, more heinously, Goldman Sachs and insiders such as John Paulson (who recently donated $400 million to Harvard) had made bets that these securities would blow up. Paulson made billions, and the media celebrated his acumen. (For an analogy, imagine the terrorists betting on 9/11 and profiting from it.) Third, to scrub salt in the wound, the big banks demanded a bailout from the very citizens whose lives the bankers had ruined! Bankers have chutzpah. In the U.S., they got hundreds of billions of dollars from the taxpayers and trillions from the Federal Reserve Bank which is nothing but a front group for the bankers.

In Greece, the domestic banks got more than $30 billion of bailout from the Greek people. Let that sink in for a moment – the supposedly irresponsible Greek government had to bail out the hardcore capitalist bankers.

Stage 3 is when the banks force the government to accept massive debts. For a biology metaphor, consider a virus or a bacteria. All of them have unique strategies to weaken the immune system of the host. One of the proven techniques used by the parasitic international bankers is to downgrade the bonds of a country. And that’s exactly what the bankers did, starting at the end of 2009. This immediately makes the interest rates (“yields”) on the bonds go up, making it more and more expensive for the country to borrow money or even just roll over the existing bonds.

From 2009 to mid 2010, the yields on 10-year Greek bonds almost tripled! This cruel financial assault brought the Greek government to its knees, and the banksters won their first debt deal of a whopping 110 billion Euros.

The banks also control the politics of nations. In 2011, when the Greek prime minister refused to accept a second massive bailout, the banks forced him out of the office and immediately replaced him with the Vice President of ECB (European Central Bank)! No elections needed. Screw democracy. And what would this new guy do? Sign on the dotted line of every paperwork that the bankers bring in.

(By the way, the very next day, the exact same thing happened in Italy where the Prime Minister resigned, only to be replaced by a banker/economist puppet. Ten days later, Spain had a premature election where a “technocrat” banker puppet won the election).

The puppet masters had the best month ever in November 2011.

Few months later, in 2012, the exact bond market manipulation was used when the banksters turned up the Greek bonds’ yields to 50%!!! This financial terrorism immediately had the desired effect: The Greek parliament agreed to a second massive bailout, even larger than the first one.

Now, here is another fact that most people don’t understand. The loans are not just simple loans like you would get from a credit card or a bank. These loans come with very special strings attached that demand privatization of a country’s assets. If you have seen Godfather III, you would remember Hyman Roth, the investor who was carving up Cuba among his friends. Replace Hyman Roth with Goldman Sachs or IMF (International Monetary Fund) or ECB, and you get the picture.

Stage 4: Now, the rape and humiliation of a nation begin. For the debt that was forced upon them, Greece had to sell many of its profitable assets to oligarchs and international corporations. And privatizations are ruthless, involving everything and anything that is profitable. In Greece, privatization included water, electricity, post offices, airport services, national banks, telecommunication, port authorities (which is huge in a country that is a world leader in shipping) etc.

In addition to that, the banker tyrants also get to dictate every single line item in the government’s budget. Want to cut military spending? NO! Want to raise tax on the oligarchs or big corporations? NO! Such micro-management is non-existent in any other creditor-debtor relationship.

So what happens after privatization and despotism under bankers? Of course, the government’s revenue goes down and the debt increases further. How do you “fix” that? Of course, cut spending! Lay off public workers, cut minimum wage, cut pensions (same as our social security), cut public services, and raise taxes on things that would affect the 99% but not the 1%. For example, pension has been cut in half and sales tax increase to more than 20%. All these measures have resulted in Greece going through a financial calamity that is worse than the Great Depression of the U.S. in the 1930s.

Of course, the ever-manipulative bankers demand immediate privatization of all media which means that the country now gets photogenic TV anchors who spew propaganda every day and tell the people that crooked and greedy banksters are saviors; and slavery under austerity is so much better than the alternative.

If every Greek person had known the truth about austerity, they wouldn’t have fallen for this. Same goes for Spain, Italy, Portugal, Ireland and other countries going through austerity.The sad aspect of all this is that these are not unique strategies. Since World War II, these predatory practices have been used countless times by the IMF and the World Bank in Latin America, Asia, and Africa.

(read the full article at Truth & Satire)

Hillary Clinton approved arms for terrorist enemies of the United States

Hillary’s secret war

By Andrew P. Napolitano

The Washington Times: July 1, 2015

In the course of my work, I am often asked by colleagues to review and explain documents and statutes. Recently, in conjunction with my colleagues Catherine Herridge and Pamela Browne, I read the transcripts of an interview Ms. Browne did with a man named Marc Turi, and Ms. Herridge asked me to review emails to and from State Department and congressional officials during the years when Hillary Clinton was the secretary of state.

What I saw has persuaded me beyond a reasonable doubt and to a moral certainty that Mrs. Clinton provided material assistance to terrorists and lied to Congress in a venue where the law required her to be truthful. Here is the backstory.

Mr. Turi is a lawfully licensed American arms dealer. In 2011, he applied to the Departments of State and Treasury for approvals to sell arms to the government of Qatar. Qatar is a small Middle Eastern country whose government is so entwined with the U.S. government that it almost always will do what American government officials ask of it.

In its efforts to keep arms from countries and groups that might harm Americans and American interests, Congress has authorized the Departments of State and Treasury to be arms gatekeepers. They can declare a country or group to be a terrorist organization, in which case selling or facilitating the sale of arms to it is a felony. They also can license dealers to sell.

Mr. Turi sold hundreds of millions of dollars’ worth of arms to the government of Qatar, which then, at the request of American government officials, were sold, bartered or given to rebel groups in Libya and Syria. Some of the groups that received the arms were on the U.S. terror list. Thus, the same State and Treasury Departments that licensed the sales also prohibited them.

How could that be?

That’s where Mrs. Clinton’s secret State Department and her secret war come in. Because Mrs. Clinton used her husband’s computer server for all of her email traffic while she was the secretary of state, a violation of three federal laws, few in the State Department outside her inner circle knew what she was up to.

Now we know.

She obtained permission from President Obama and consent from congressional leaders in both houses of Congress and in both parties to arm rebels in Syria and Libya in an effort to overthrow the governments of those countries.

Many of the rebels Mrs. Clinton armed, using the weapons lawfully sold to Qatar by Mr. Turi and others, were terrorist groups who are our sworn enemies. There was no congressional declaration of war, no congressional vote, no congressional knowledge beyond fewer than a dozen members, and no federal statute that authorized this.

When Sen. Rand Paul, Kentucky Republican, asked Mrs. Clinton at a public hearing of the Senate Armed Services Committee on Jan. 23, 2013, whether she knew about American arms shipped to the Middle East, to Turkey or to any other country, she denied any knowledge. It is unclear whether she was under oath at the time, but that is legally irrelevant. The obligation to tell the truth, the whole truth and nothing but the truth to Congress pertains to all witnesses who testify before congressional committees, whether an oath has been administered or not. (Just ask Roger Clemens, who was twice prosecuted for misleading Congress about the contents of his urine while not under oath. He was acquitted.)

(read the relevant testimony and the rest of the article at The Washington Times)

At the time that Mrs. Clinton denied knowledge of the arms shipments, she and her State Department political designee, Andrew Shapiro, had authorized thousands of shipments of billions of dollars’ worth of arms to U.S. enemies to fight her secret war. Among the casualties of her war were U.S. Ambassador to Libya Chris Stevens and three colleagues, who were assassinated at the American consulate in Benghazi, by rebels Mrs. Clinton armed with American military hardware in violation of American law.

This secret war and the criminal behavior that animated it was the product of conspirators in the White House, the State Department, the Treasury Department, the Justice Department, the CIA and a tight-knit group of members of Congress. Their conspiracy has now unraveled.

(read the full article at The Washington Times)

…

Alternative Free Press – fair use-

The Global Template for Collapse: The Enchanting Charms of Cheap, Easy Credit

Charles Hugh Smith

Of Two Minds : June 29, 2015

Cheap, easy credit has created moral hazard and nurtured magical thinking throughout the global economy.

According to polls, the majority of Greek citizens want the benefits of membership in the euro/EU and the end of EU-imposed austerity. The idea that these are mutually exclusive doesn’t seem to register.

This is the discreet charm of magical thinking: it promises an escape from the difficulties of hard choices, tough trade-offs, the disruption of vested interests and most painfully, the breakdown of the debt machine that has enabled the distribution of swag to virtually everyone in the system (a torrent to those at the top, a trickle to the majority at the bottom, but swag nonetheless).

If we had to summarize the insidious charm of magical thinking, we might start with the overpowering appeal of using credit to ease all difficulties.

Need money to fund various healthcare/national defense rackets? Borrow the money. Need to keep people employed building ghost cities in the middle of nowhere? Borrow the money. Need to keep buying shares of the company’s stock to push the value of each share ever higher? Borrow the money.

The problem with cheap, easy credit is Cheap, easy credit destroys discipline. The lifetime costs of debt taken on to fund bridges to nowhere, healthcare/national defense rackets, ghost cities, stock buybacks, etc. are never calculated. The opportunity costs are also never calculated.

When credit is costly and hard to get, marginal borrowers can’t get loans and nobody dares borrow at high rates of interest for low-yield, high-risk schemes. When credit is costly and hard to get, what doesn’t pencil out doesn’t get funded.

When credit is cheap and easy to get, every scheme and racket gets funding because hey, why not? The cost is low (at the moment) and the gain might be fantastic. But even if the gain is unknown, the kickback/campaign contributions make it worthwhile even if the scheme fails.

Professional economists are duty-bound to claim national economies are not merely extensions of households. But this is just another falsity passed off as sophisticated truth by a profession that is being discredited by the reality of its failed policies, failed theories and failed predictions.

Since human psychology remains the dominant force in all economics, the household and national economies can only differ in scale.

In the 1970s, credit was scarce and hard to get. Young workers qualified for a $300 limit credit card, and it took careful management of that responsibility (always paying on time, etc.) to get a meager increase to $500. Mortgage rates were high (10%+) and your income and household balance sheet were scrutinized before any lender took a chance on lending you tens of thousands of dollars to buy a house. After all, the bank would be stuck with the losses if you defaulted.

Then came financialization. Banks could skim the profits from originating loans and offload the risk of default onto towns in Norway, credulous pension funds and other greater fools.

And if a default threatened the bank–for example, Greece in 2011–the bank simply bought political power and shifted the debt onto taxpayers. “The ATMs will stop working,” the bankers threatened their political flunkies in Congress in 2008, and the bought-and-paid-for toadies in Congress and the Federal Reserve obediently shifted trillions of dollars in private liabilities and sketchy debt-based “assets” such as mortgages onto the taxpayers and the Fed balance sheet.

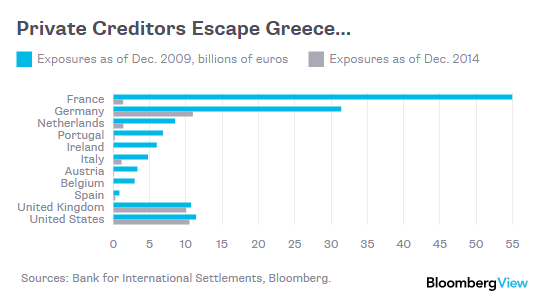

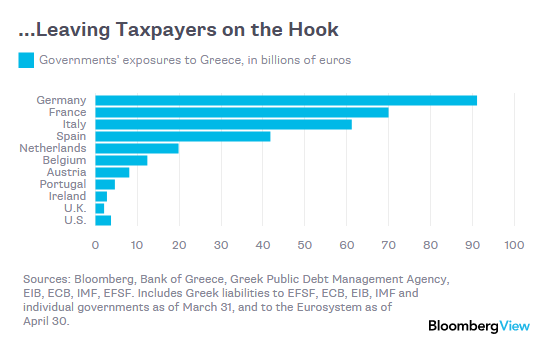

The same transfer of risk and losses occurred in Europe, as these charts demonstrate: (Source: If Greece Defaults, Europe’s Taxpayers Lose)

Here is the debt in 2009–mostly owed to private banks and bondholders:

Here is the debt in 2015–almost all was shifted onto the backs of taxpayers:

Ask yourself this: if you could shift risk and losses to the taxpayers, how would that affect your investing/gambling? Wouldn’t you take much higher risks, knowing that losses would not fall to you but to abstract taxpayers? Of course you would, and this is the essence of moral hazard–the disconnect of risk and consequence.

Cheap, easy credit has created moral hazard and nurtured magical thinking throughout the global economy. The heart of magical thinking is that consequences have been disappeared or shifted onto others by financial enchantment.

(Read the full article at of two minds)